April WASDE Analysis

Initial Takeaways

April’s WASDE landed with a thud for wheat bulls and offered little fresh ammunition for corn or soybean traders. We remain firmly in Golden Grain Cycle Stage #1, where prices continue chopping sideways around cost-of-production levels, waiting for a catalyst that hasn’t arrived. The report’s biggest surprise came in wheat, where stocks blew past estimates and climbed to their highest level since 2019/20. With South American harvest pressure on soybeans and U.S. planting season ramping up, the market’s attention will soon pivot from old crop accounting to weather and new crop development.

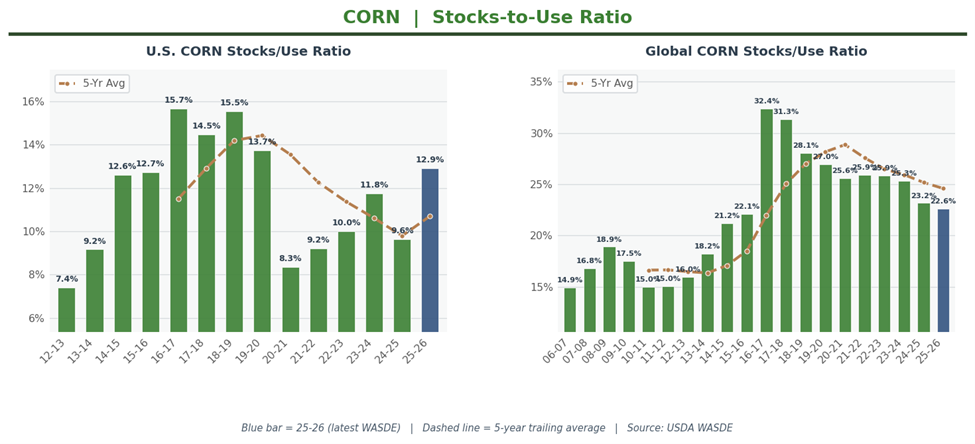

CORN

USDA made no changes to the U.S. corn balance sheet this month. Ending stocks held at 2.127 billion bushels, a hair below the 2.131 billion that analysts expected. Feed and residual use stayed put at 6.2 billion bushels, though first-half disappearance of 9.6 billion bushels ran more than a billion above last year’s pace. That’s constructive, but the market already priced it in.

The season-average price ticked up 5 cents to $4.15 per bushel. U.S. stocks-to-use sits at 12.91%, squarely in adequate territory: not tight enough to spark a rally, not burdensome enough to crush prices further.

Global corn stocks came in at 294.81 million metric tons, above the 293.2 mmt estimate. World stocks-to-use at 22.64% reflects comfortable supplies internationally. Nothing here to move the needle.

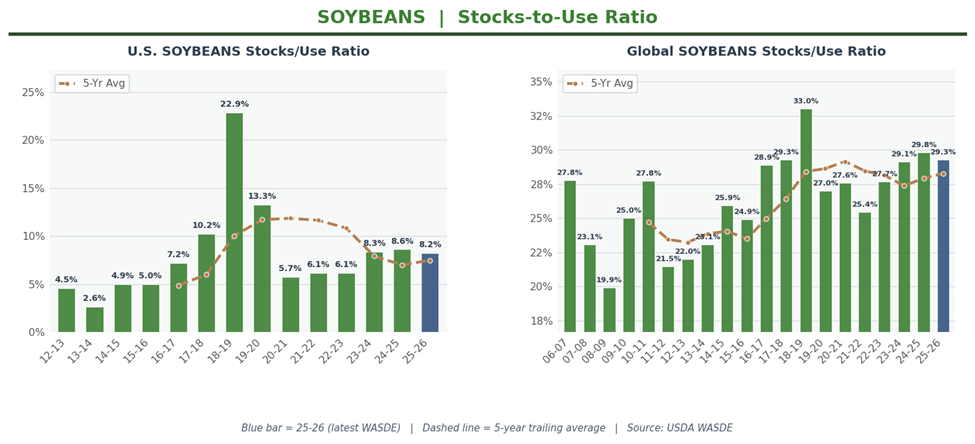

SOYBEANS

The soybean balance sheet featured a notable shuffle: USDA raised crush 35 million bushels to 2.61 billion while cutting exports by the same amount to 1.54 billion. Strong domestic meal demand is absorbing beans that aren’t finding their way onto ships, thanks largely to aggressive South American shipments stealing market share. Ending stocks held unchanged at 350 million bushels, essentially matching the 349 million estimate.

The USDA adjusted higher the season-average price forecasts across the complex. Beans gained 10 cents to $10.30 per bushel, meal jumped $10 to $310 per short ton, and oil added 4 cents to 59 cents per pound.

U.S. stocks-to-use at 8.21% remains tight by historical standards. Below 10% leaves little margin for any production hiccup or demand surge. Global stocks came in at 124.79 mmt, slightly under the 125.5 mmt estimate. World stocks-to-use at 29.3% sits just below the burdensome threshold but continues trending lower. The domestic crush story is quietly bullish; the export story is not.

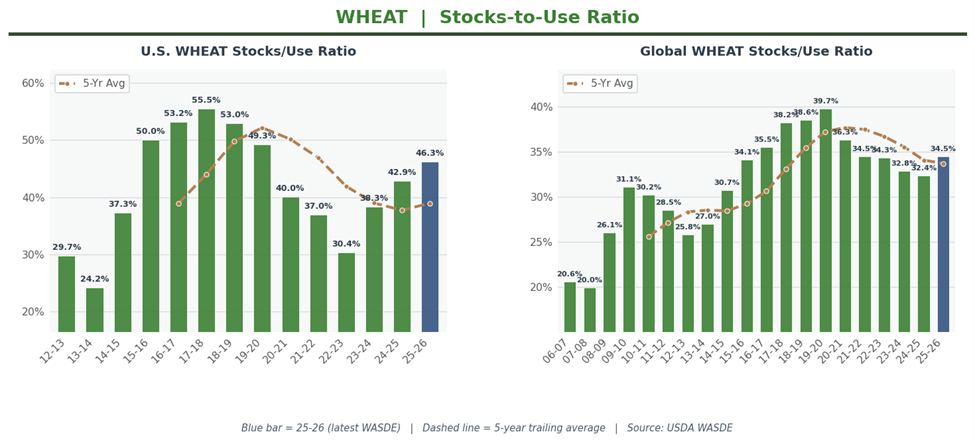

WHEAT

Wheat bears got their report. U.S. ending stocks jumped to 938 million bushels, 15 million above the 923 million estimate and 10% higher than last year. This marks the largest carryout since 2019/20. Supplies grew on higher imports (Census data through February confirmed the inflows), while seed use fell based on the Prospective Plantings report. Exports held at 900 million bushels.

U.S. stocks-to-use at 46.28% is unambiguously burdensome: nearly half a year’s worth of wheat sitting in storage. Yet USDA still raised the season-average price 5 cents to $5.00 per bushel.

Globally, stocks ballooned to 283.12 mmt, a full 5.72 mmt above the 277.4 mmt estimate. World stocks-to-use at 34.52% confirms ample supplies everywhere you look. Demand simply isn’t rationing these stocks at current prices.

Weather scares and fertilizer availability, in our view remain wheat’s only path higher from here.

Past performance is not indicative of future results. This commentary is for informational purposes only and does not constitute investment advice. Commodity investments involve substantial risk of loss.