June WASDE Analysis

Initial Takeaways

June WASDE reports rarely move the needle, and this one mostly held to script. USDA left the U.S. corn and soybean balance sheets virtually untouched and confined the action to old-crop bookkeeping. Wheat carried what little news there was, and it cut both ways: a smaller new-crop production figure and a carryout 20 million bushels below the analyst average, paired with a 50-cent cut to the season-average price forecast.

We remain in Golden Grain Cycle Stage #1, with prices chopping around cost-of-production. May’s report tested the ceiling. June took some of the pressure off, particularly in global corn, where bigger South American and Indian crops rebuilt part of the cushion. Summer weather and the June 30 Acreage report are the next gating factors.

CORN

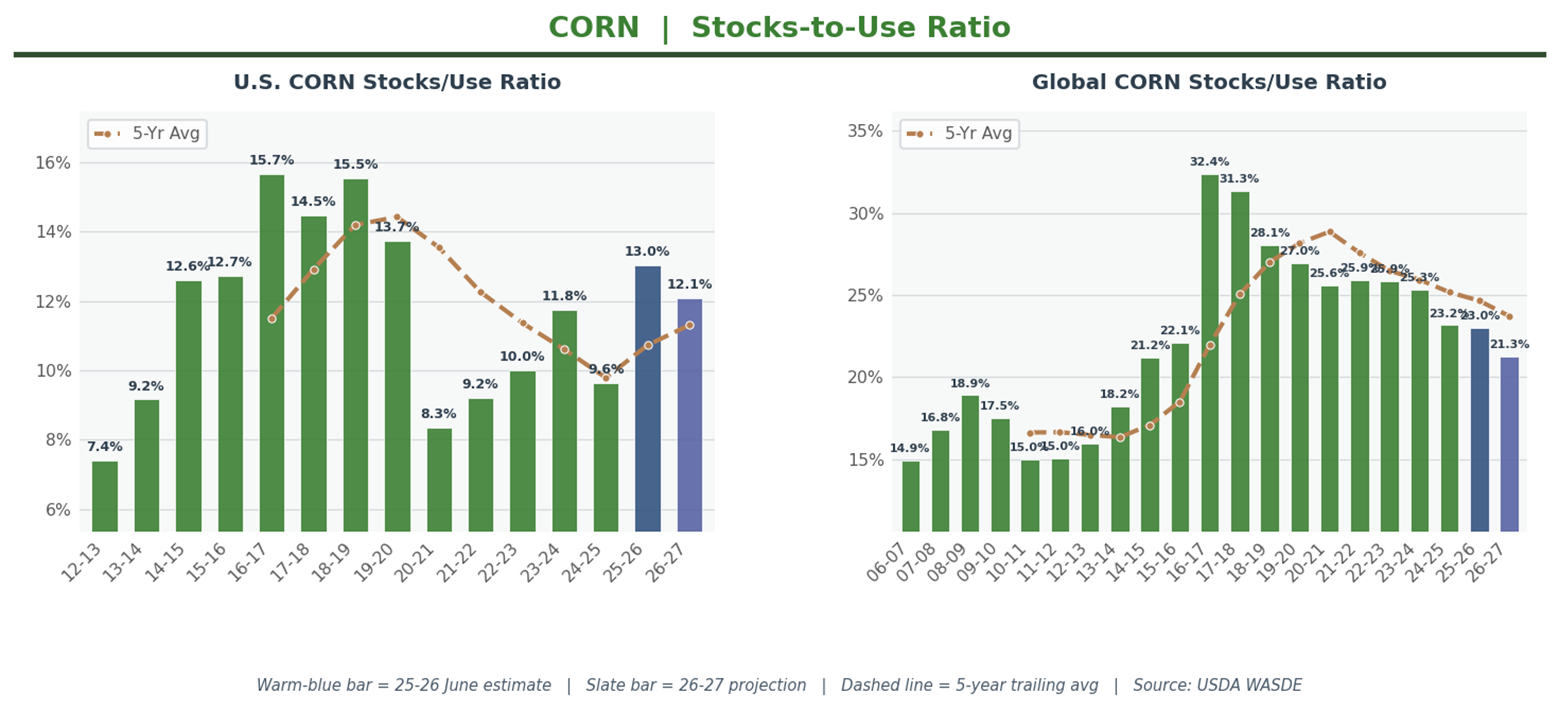

USDA nudged 2025/26 U.S. corn carryout up 3 million bushels to 2,145 million, 8 above the 2,137-million analyst average. The change nets out small adjustments to imports, ethanol use, and exports based on data to date. The 2025/26 season-average price forecast held at $4.15 per bushel.

New crop was a copy of May. Production held at 15,995 million bushels on a 183.0 bushel-per-acre yield, both within a hair of consensus (15,989 and 182.9). Ending stocks ticked up 3 million to 1,960 million, 13 above the 1,947-million analyst average. The 2026/27 season-average price forecast held at $4.40 per bushel. U.S. new-crop stocks-to-use holds at 12.1%.

The global outlook is where June pushed back on May’s bullish print. USDA raised 2025/26 world ending stocks 6.4 mmt to 303.36 million metric tons, with India (sharply higher area and yield per the latest government data), Brazil, Argentina, and Paraguay all producing more than previously estimated. That bigger old-crop cushion carried forward: 2026/27 world ending stocks moved up 3.7 mmt to 281.22 million. The figure still points to the tightest global corn carryout in over a decade, but the direction this month was looser, not tighter. World new-crop stocks-to-use sits at 21.3%, up from 21.1% in May.

SOYBEANS

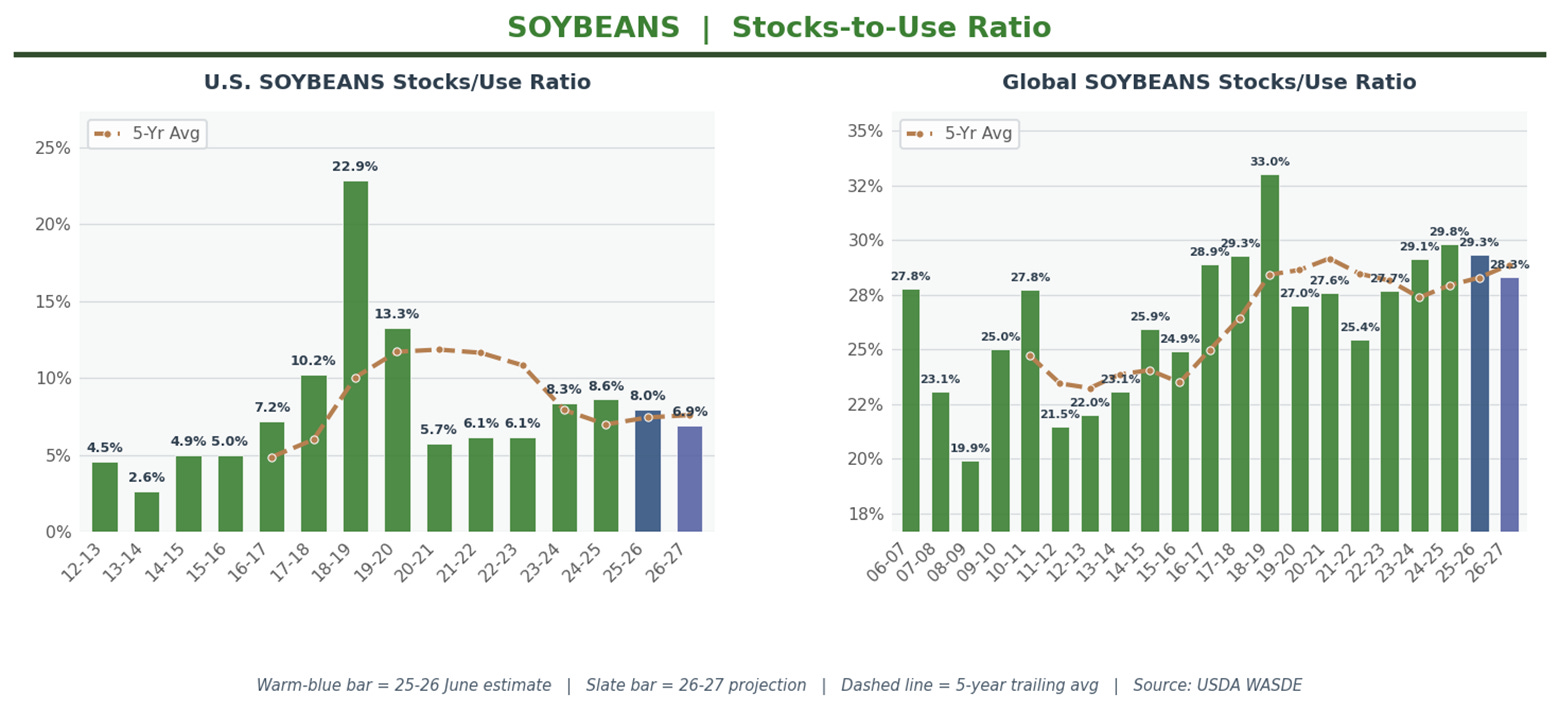

USDA didn’t touch the 2026/27 U.S. soybean balance sheet. Ending stocks held at 310 million bushels, right on top of the 311-million analyst average. Production stays at 4,435 million bushels on a 53.0 yield, crush holds at 2,750 million, and exports hold at 1,630 million. The 2026/27 season-average price forecasts were unchanged: $11.40 per bushel for soybeans, 70 cents per pound for oil, and $310 per short ton for meal. New-crop stocks-to-use at 6.9% remains very tight.

The old-crop action was all demand-side reshuffling. Crush moved up another 20 million bushels to 2,650 million on stronger meal exports and domestic disappearance, while exports dropped 20 million to 1,510 million based on Census data to date. The two offset, leaving 2025/26 ending stocks unchanged at 340 million bushels, in line with the 339-million analyst average. Soybean oil used for biofuel was raised for 2025/26 to 14.55 billion pounds. The 2025/26 season-average price forecast held at $10.40 per bushel. Old-crop stocks-to-use at 8.0% sits below the 10% line that historically starts to support prices.

Globally, 2026/27 ending stocks edged up 0.1 mmt to 124.88 million metric tons, mainly on Argentina, whose 2025/26 crop was raised 2 mmt to 50 million tons. Brazil’s 2026/27 crop held at 186 mmt. World new-crop stocks-to-use eases to 28.3% from 29.3% in the old crop.

WHEAT

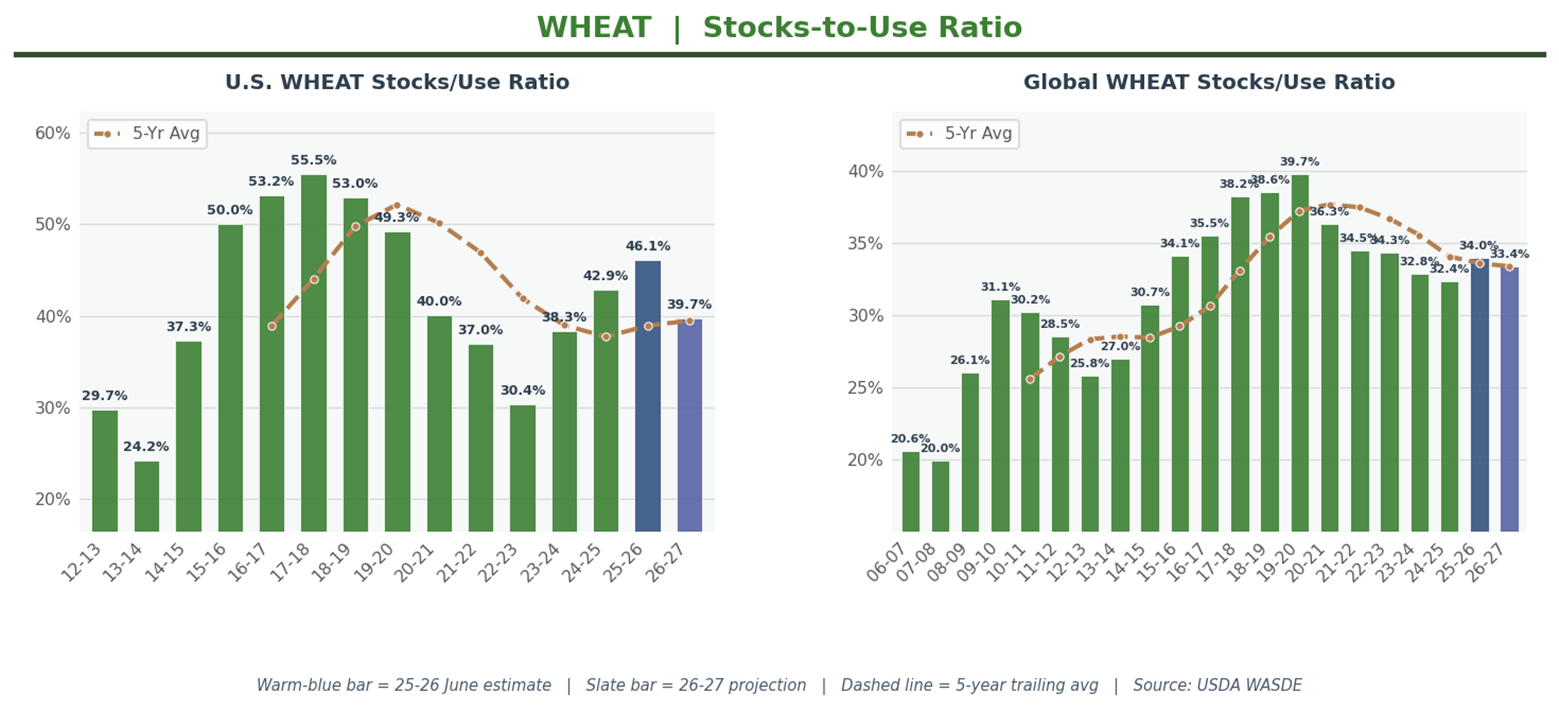

Wheat carried the report’s only real news. USDA lowered 2026/27 all-wheat production 18 million bushels to 1,543 million, largely on smaller Hard Red Winter output reported in the June 11 Crop Production release. The all-wheat yield dropped half a bushel to 47.0 bushels per acre. With no other balance sheet changes, new-crop ending stocks fell 18 million to 744 million bushels, 20 below the 764-million analyst average and 20% under 2025/26. New-crop stocks-to-use steps down to 39.7%.

Then the other edge: USDA cut the 2026/27 season-average price forecast 50 cents to $6.00 per bushel, citing expectations for futures and cash prices over the marketing year. A smaller crop and a lower price forecast in the same table suggests USDA may see burdensome old-crop supplies, not new-crop production, setting the price for now.

Old-crop ending stocks held at 935 million bushels, 7 below the 942-million analyst average. The 2025/26 season-average price forecast nudged up a nickel to $5.05. Old-crop stocks-to-use at 46.1% is still unambiguously burdensome.

Globally, 2026/27 ending stocks were raised 0.4 mmt to 275.42 million metric tons. Production gains for Russia (up 2.0 mmt to 88.0 on near-ideal weather), Turkey (up 1.5 to a record 22.5), and Ukraine (up 0.5 to 23.5) more than offset a 2.0 mmt cut to Australia. World new-crop stocks-to-use holds at 33.4%, tightening modestly from 34.0% in the old crop but still burdensome by historical standards.