Month-End Selling Hits the Complex, Beans Hold the Line

Grains & Sugar Weekly

Month-end caught up with the grain complex this week. Funds liquidated longs into Friday, Iran-deal headlines pulled the energy and fertilizer premium out of the board, and a fast U.S. planting season stripped away what was left of the weather bid. Wheat took the worst of it. Soybeans were the one holdout.

Corn:

The September contract drifted down to around $4.63 a bushel by Friday, well off the early-May spike near $4.90. The September contract fell about 1.9% on the day to $4.47.

USDA’s Crop Progress report had 86% of the U.S. corn crop in the ground as of May 25, on par with last year, a quick pace that pulled the weather-risk premium back out of the board.

Funds noticed. Money managers cut their net-long corn position by 87,850 contracts to 205,504, the least bullish in five weeks, while short-only bets climbed to a 12-week high. Export sales of 1.634 million tons undershot the prior week’s 2.407 million, though they topped the survey. Underneath the tape, farm economics stayed ugly: the National Corn Growers Association pegged grower losses near $100 an acre on elevated fertilizer and diesel costs tied to the Iran war.

There was a midweek bounce when NOAA’s 8-to-14-day outlook turned drier for the Plains and Midwest, and traders are increasingly eyeing a developing El Nino, which StoneX calls the primary forward focus for the grain complex. The sharper tell came from Charlie Sernatinger’s desk at Marex: anyone who bought corn in May is now underwater, which sets up more long liquidation. A year ago nearby corn sat at $4.40, only twenty cents cheaper than today. With four million fewer acres planted, the long-term bulls likely don’t see much downside from here.

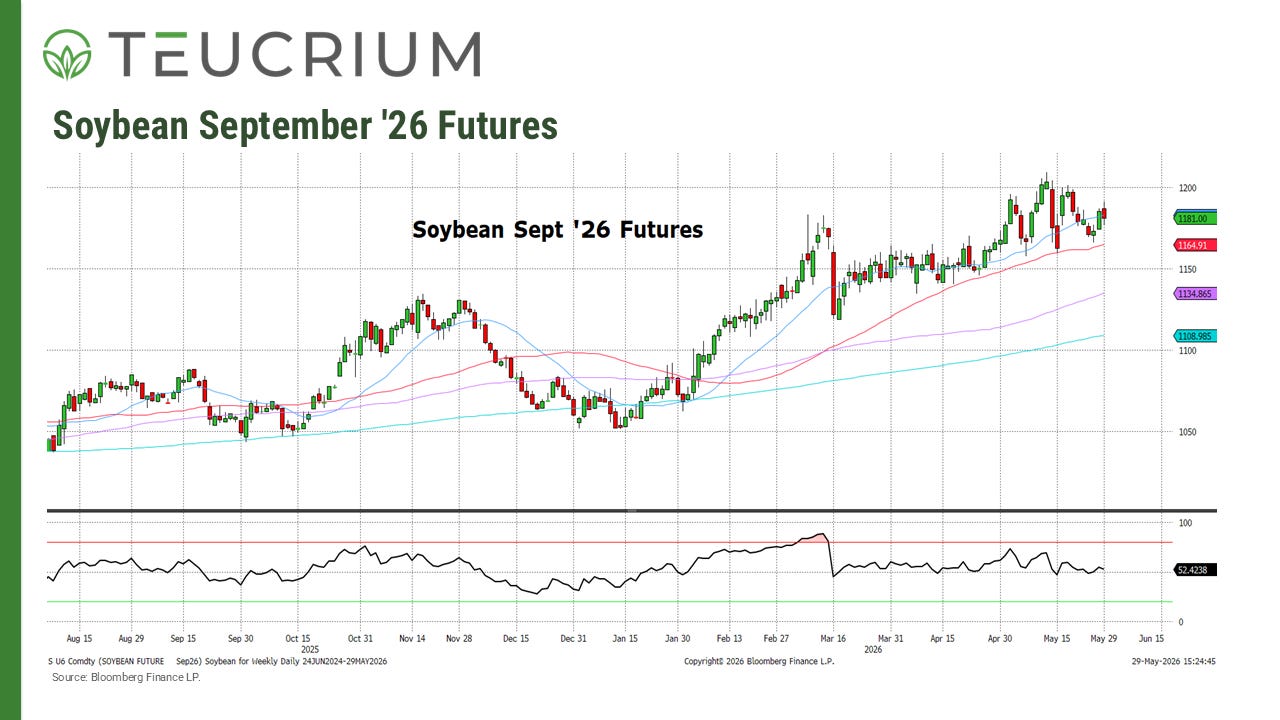

Soybeans:

Soybeans refused to break. The September contract held near the upper end of its range and finished the week at $11.81. Support came from soy oil, which pushed to contract highs on a biofuels bid. Brian Grete of Commstock Investments noted that funds kept trimming their grain longs, with the exception of soyoil.

The demand read helped. A Bloomberg survey put April soybean crush at 214.8 million bushels, up 6.1% year-over-year, with the USDA Fats and Oils report due June 1. Planting ran ahead of schedule at 79% done, four points clear of last year, so weather anxiety stayed muted. Even so, funds de-risked here too, cutting their net-long by 18,252 contracts to 189,552, the least bullish in four weeks.

Sernatinger’s desk flagged the tension worth watching. The July/November spread keeps sliding toward a carry after trading at a 76-cent inverse back in March, and the bean/corn ratio has run from 2.5 to 2.62. When the flat price holds firm while the spread structure rolls over, in our view the resilience could be living on borrowed time.

Wheat:

Wheat was the biggest loser on the week. The September contract broke down to roughly $6.23 from weekly highs near $6.60. The move was wheat’s steepest drop in more than nine months, with the September contract off ~ 4.5%.

The trigger was easing drought worry. Saxo Bank’s Ole Hansen said prices retreated as concerns about drought in major producing regions eased and harvest prospects improved.

Here is the strange part. The U.S. winter wheat crop is in historically poor shape, just 26% rated good-to-excellent, a record low for the date, with Kansas facing what some call its worst crop since 1972 and 70% of the winter wheat area sitting in drought. The tape sold it anyway. Money managers boosted their net-short Chicago position by 13,907 contracts to 18,706, with shorts at a 14-week high.

Global supply swamped the crop story. Russia expects to export 60 million tons of grain this marketing year, including 50 million of wheat, well above prior forecasts. India is headed for a record 120.66-million-ton crop. Rabobank sees Australia’s next harvest falling 41% to 21.3 million tons, a bullish 2026/27 signal, though a distant one.

Sugar:

Sugar also sold off this week before reversing on Friday. October contract hit it’s lowest level since April on Thursday before rallying to close back above 1450 cents on Friday.

The bearish weight came from Brazil. UNICA reported Center-South mills crushed 40.1 million tons of cane in the second half of April, more than double a year ago, with sugar output at 1.80 million tons against 859,000. Mills are front-loading the crush ahead of a possible El Nino.

The cane mix is the swing variable. Brazilian mills sent 40.3% of cane to sugar, below some projections, as ethanol economics pulled hard. Green Pool widened its 2026/27 global deficit estimate to 4.3 million tons from 1.66 million on that ethanol shift.

India sits on the other side of the trade. India’s export ban runs through September 30, and the weather office cut its monsoon forecast to 90% of the long-term average (down from 92%), the spark for Friday’s rally.

Funds stayed heavily short, boosting their net-short raw position by 19,768 contracts to 111,538, the most bearish in four weeks. That short base is fuel. As Citi’s Arkady Gevorkyan put it, the optimism now hinges on how El Nino develops.